Localising Forward Intensities for Multiperiod Default

-

- 0 Rating

- 0 Reviews

- 3 Students Enrolled

Localising Forward Intensities for Multiperiod Default

Localising Forward Intensities for Multiperiod Default

-

- 0 Rating

- 0 Reviews

- 3 Students Enrolled

Courselet Content

Requirements

- None

General Overview

Description

This talk has been recorded at Summer Camp 2022.

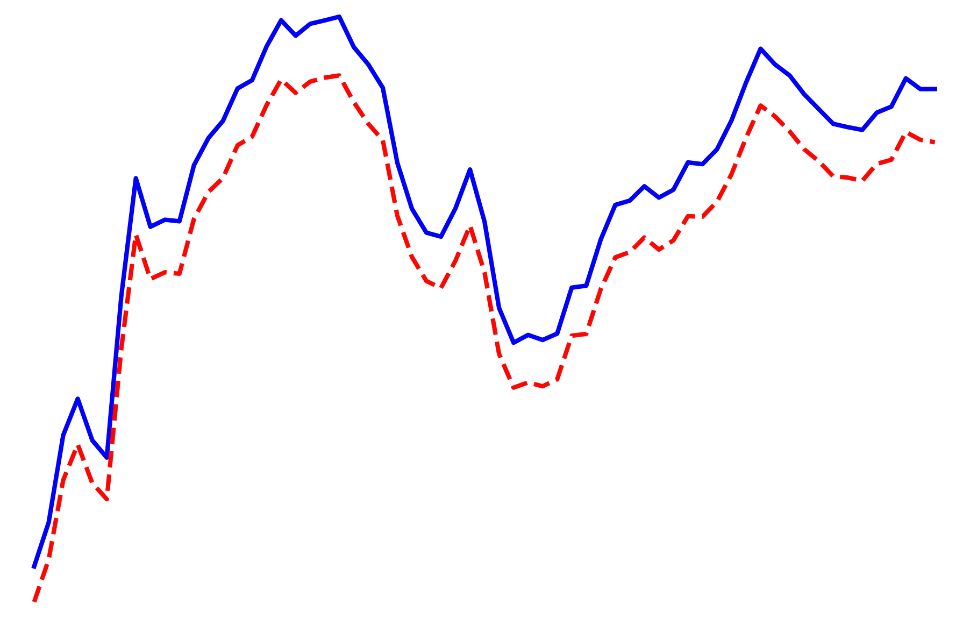

The talk represents our research in which using an adaptive Forward Intensities Approach (FIA), we investigate mutiperiod corporate defaults and other delisting schemes. The proposed approach is fully data-driven and is based on adaptive estimation and the selection of optimal estimation windows. Time-dependent model parameters are determined by a sequential testing procedure. This makes this approach adaptive at every time point. Applying the proposed method to monthly data on 2000 U.S. public firms over a sample period from 1991 to 2011, we estimate default probabilities over various prediction horizons. The prediction performance is evaluated against the global FIA that employs all past observations. For the six months prediction horizon, the local adaptive FIA performs with the same accuracy as the benchmark. The default prediction power is improved for the longer horizon (one to three years). Our method can be applied to any other specifications of forward intensities.

Recommended for you

Meet the instructors !

.jpg)

Kainat Khowaja is currently a research associate and PhD student at Humboldt University of Berlin with International Research Training Group IRTG1792 “High dimensional non stationary time series analysis”.

Along with a double masters degree in Mathematics and high international exposure through various exchanges. she has a rich background in research, scientific presentations and teaching. Since 2015, she has worked as a teaching assistant for 4+ courses and completed various research projects related to statistics, econometrics, machine learning and finance. She has also co-taught four graduate level courses related to smart data analysis and mathematical statistics at her current institute.

Presently, she is working on the methodology to construct uniform confidence bands around non-parametric estimates from generalized random forests with assistance of multiplier bootstrap. Her work extends on the scope in which mathematical properties can be utilized to bridge the gap between theoretical understanding of random forests and their practical performance. Her research interests include interpretability of and variable selection through random forests and she would like to continue her research in the same area.