DArLiQ Dynamic Autoregressive Liquidity

-

- 4.9 Rating

- 3 Reviews

- 3 Students Enrolled

DArLiQ Dynamic Autoregressive Liquidity

A new semiparametric model for the Amihud illiquidity measure

-

- 4.9 Rating

- 3 Reviews

- 3 Students Enrolled

Requirements

- None

General Overview

Description

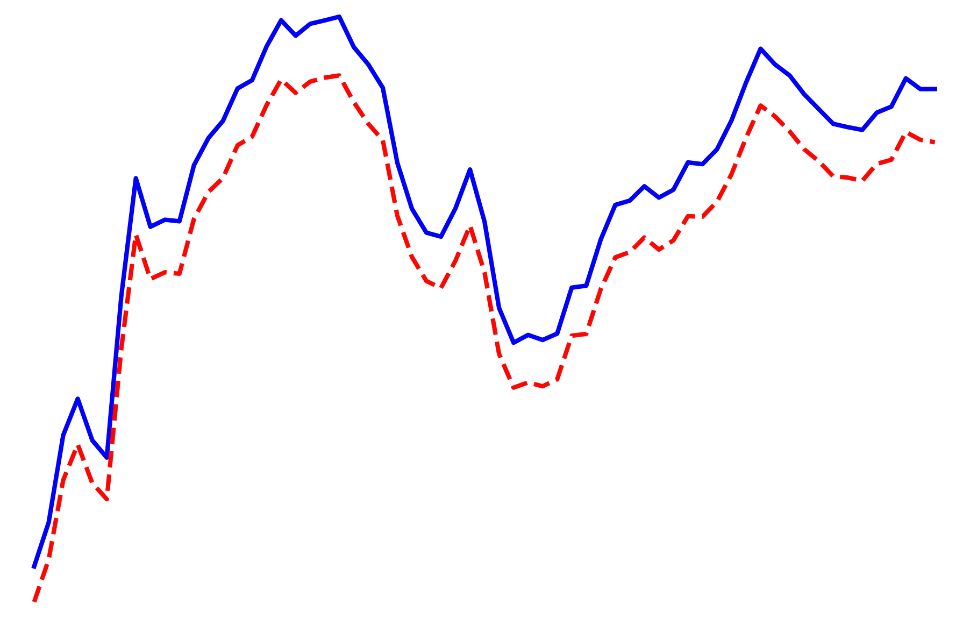

We introduce a dynamic semiparametric multiplicative error model (MEM) for the Amihud illiquidity measure and develop a GMM estimator based on moment restrictions and a semiparametric maximum likelihood procedure. We investigate the link between stock market excess returns and different components of illiquidity. We propose tests to detect both permanent and temporary breaks in illiquidity.

Recommended for you

Meet the instructors !

Linqi Wang is currently a postdoc researcher at the Faculty of Economics, University of Cambridge. Prior to that, she was a PhD student in Statistics (specializing in financial econometrics) at the Université catholique de Louvain.

Her research interests concentrate on various topics in financial econometrics, with a focus on developing new modelling approaches to better capture the key features of financial time series data. In particular, she focuses on the measurement and estimation of volatility, correlation, and liquidity with applications to portfolio allocation, risk management, and asset pricing.